Software-First Innovations for Under-Digitized Infrastructure

An Industry Report

This report was my capstone project for the Girls Into VC Fellowship. Thank you to my mentors and peers for all their support during this research process!

I. Introduction

The Importance of Software-First Innovation in Infrastructure

As climate volatility, aging assets and workforce, and rapid urbanization intensify, the demand for modern, resilient infrastructure has never been greater. Recent estimates suggest a multi-trillion-dollar gap between current infrastructure investment and what is needed to maintain growth and resilience over the coming decades. Sectors like water, utilities, construction, and the built environment face mounting operational and regulatory pressures that legacy systems were not designed to handle.

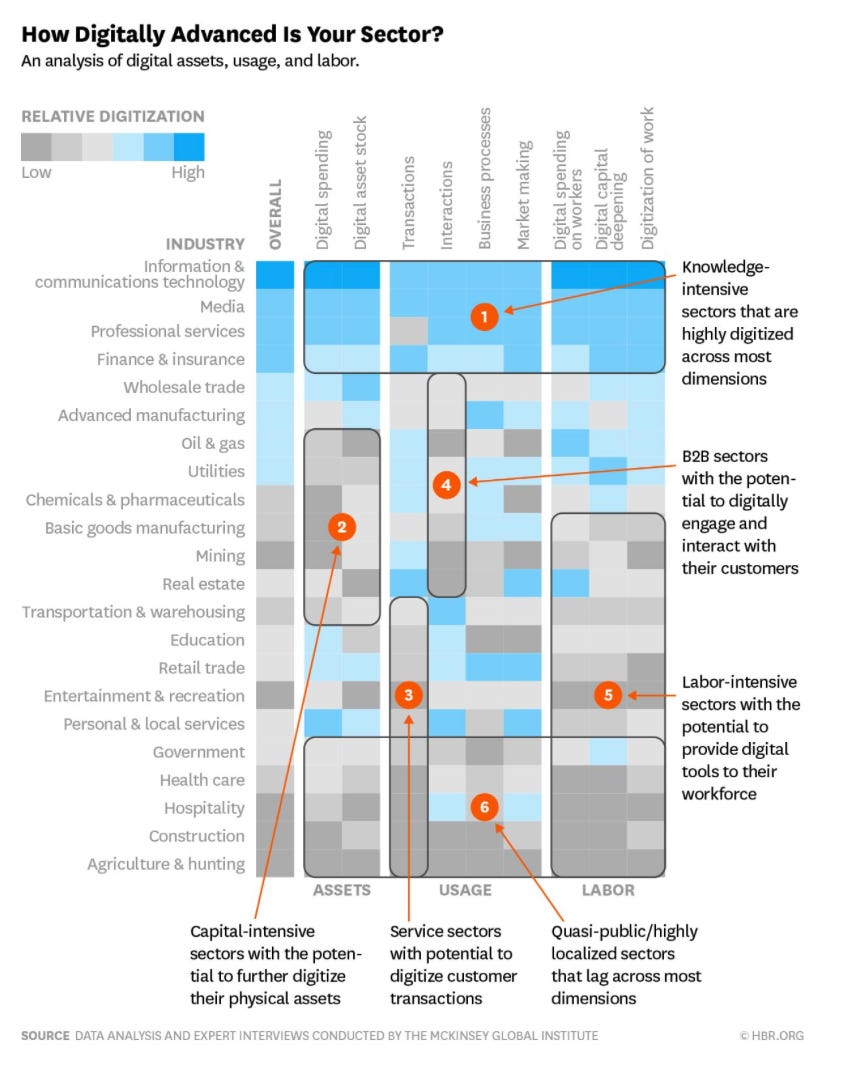

Despite their central role in society, these sectors remain among the least digitized in the global economy. Paper-based processes, fragmented data, and aging legacy systems create inefficiencies, slow response times, and limited visibility into critical infrastructure performance. As illustrated in Figure 1, sectors such as construction, utilities, and parts of the built environment rank among the least digitized across assets, usage, and labor.

In response, a new wave of software-first solutions is emerging across these infrastructure-heavy sectors. Industry analyses on construction and infrastructure repeatedly highlight digital tools, data platforms, and AI-enabled systems as core levers for closing productivity gaps and improving project outcomes. In parallel, climate-tech market trackers and recent funding rounds in AI-based climate and grid software point to growing investor interest in digital infrastructure tools that can forecast risk, optimize assets, and support real-time decision-making.

Compared with hardware-heavy infrastructure upgrades, software-first products, particularly SaaS and data platforms, can scale more quickly across fragmented customers, layer on top of existing assets, and compound value as more operational data flows through them.

Why Software-First innovation and why for under-digitized infrastructure?

Over the past decade, the technological foundations required for software-first infrastructure modernization have reached a level of maturity that enables real deployment at scale. Cloud-native platforms can now integrate with legacy systems, low-cost sensors generate continuous streams of operational data, and advances in AI and geospatial analytics allow for real-time understanding of physical assets that historically remained offline. At the same time, regulatory drivers, from climate disclosure requirements to infrastructure resilience mandates, have increased the economic incentives for operators to adopt digital tools.

In this report, “software-first” refers to tools where the primary value creation comes from digital workflows, data platforms, and AI-driven analytics rather than physical hardware. These products often integrate with existing infrastructure, rather than replacing it , and scale through standardized deployments across utilities, contractors, or facility networks. Importantly, software-first approaches also compound in value over time as they accumulate operational data, refine predictive models, or integrate more deeply into field and back-office workflows. This accumulation of proprietary operational data creates meaningful switching costs and reinforces the competitive moat of platform providers over time.

What this report aims to do

This industry report maps the emerging landscape of software-first innovation across water, utilities, construction, and the built environment. It outlines the most active software categories, examines funding and valuation trends, and highlights the criteria investors use to evaluate companies operating in these historically overlooked sectors. Drawing on sector reports, venture datasets, and case studies, it identifies where digital infrastructure is gaining traction and where the next wave of opportunity is likely to emerge.

II. Mapping the Software Landscape in Under-Digitized Sectors

To understand how software-first innovation is reshaping under-digitized infrastructure, it’s useful to categorize the major types of digital solutions emerging across water, construction, utilities, and industrial operations. While each sector has unique constraints, several common software patterns have started to define the next generation of infrastructure technology.

Water Infrastructure Software

Water utilities are among the most operationally complex and fragmented infrastructure operators in the U.S., with more than 50,000 public water systems and widely varying levels of technical capacity. As a result, workflows (such as asset management, leak detection, and compliance reporting) often rely on paper logs and disconnected spreadsheets, aging SCADA systems, and institutional memory. Software-first tools are emerging to modernize these functions by providing centralized asset management, GIS-driven network visibility, real-time monitoring, and automated reporting workflows.

SaaS platforms such as Ziptility help utilities manage assets, track maintenance, and improve field operations. AI inspection tools such as SewerAI use computer vision and machine learning to automate defect detection in sewer inspection videos, accelerating workflows that have historically been manual and time-intensive. Geospatial planning tools like CivilGrid integrate mapping, underground utility data, and permitting requirements to streamline project planning and reduce the risk of hitting unmarked assets. Real-time water quality and leak detection platforms leverage sensors and cloud analytics to help utilities reduce water loss and respond rapidly to operational anomalies. As regulators increase pressure on utilities to meet resilience, safety, and reporting requirements, digital water platforms are becoming foundational components of modern water system management.

Construction & Built Environment Software

Construction remains one of the least digitized industries globally, with persistent challenges such as cost overruns, scheduling delays, rework, and documentation errors. Given the sector’s high reliance on distributed contractors and field teams, software-first solutions are emerging as the most scalable way to standardize workflows, improve documentation, and increase transparency across project stakeholders. Digital tools are particularly suited to construction because they replace manual processes rather than physical assets, allowing software layers to scale across thousands of projects with relatively low friction.

Workflow software such as Procore centralizes project communication, documentation, scheduling, and budgeting. Computer vision platforms like OpenSpace and HoloBuilder automate site capture and progress tracking, creating defensible datasets that reduce disputes and rework. And again, tools such as CivilGrid provide underground mapping and permitting intelligence, helping contractors assess site conditions and avoid costly conflicts with buried infrastructure. More advanced solutions integrate digital twins and Building Information Modeling (BIM), enabling real-time coordination between architects, contractors, and facility operators. Together, these platforms help construction stakeholders reduce uncertainty, improve productivity, and create more reliable data flows across the built environment lifecycle.

Utilities & Grid Software

Electric utilities are undergoing rapid transformation as distributed energy resources (DERs), such as rooftop solar, battery storage, and electric vehicles, create far more dynamic load patterns than traditional grid systems were designed to manage. Historically, grid visibility relied on limited sensors and legacy SCADA systems that offered only partial situational awareness. As the grid becomes more complex and climate events more frequent, software-first solutions are emerging as the “intelligent layer” that enables forecasting and real-time decision-making.

AI-based forecasting platforms like Amperon provide granular, real-time load predictions that help utilities balance supply and demand more accurately. Distributed energy management tools such as Voltus and other Virtual Power Plant (VPP) platforms help orchestrate DER participation in grid markets. Software suites for SCADA modernization, outage management, and predictive analytics integrate directly with legacy utility infrastructure, offering enhanced visibility without requiring costly hardware overhauls. With regulators pushing for grid resilience, decarbonization, and DER integration, digital utility platforms are becoming essential components of next-generation grid operations.

Industrial Operations & Built-Environment Maintenance Software

Industrial facilities, commercial buildings, and campus environments often operate large fleets of mechanical and electrical systems that require frequent maintenance to avoid failures, energy waste, and downtime. Historically, these operations relied on analog processes and operator intuition, making maintenance reactive rather than predictive. Software-first approaches—particularly those using IoT, AI, and cloud analytics—are transforming facility operations by enabling continuous monitoring, early failure detection, and streamlined workflows.

Predictive maintenance platforms like Augury use vibration analysis and machine learning to detect equipment issues before they escalate, which reduces unplanned downtime and repair costs. Computerized maintenance management systems (CMMS) such as Fiix or UpKeep digitize work orders, asset histories, and technician workflows. IoT-enabled building analytics platforms integrate data from HVAC systems, meters, and sensors to optimize energy use and identify anomalies. AI-driven failure detection models can detect subtle patterns in equipment behavior, enabling data-driven maintenance strategies. As buildings and industrial facilities aim to reduce energy consumption and improve operational resilience, these digital systems provide a scalable path to smarter, more efficient asset management.

Together, these categories illustrate the breadth of software-first innovation reshaping traditionally analog and operationally intensive sectors. Although each vertical addresses different challenges, they share common characteristics: 1) integration into existing workflows, 2) reliance on accumulating data, and 3) the ability to scale across fragmented markets with minimal physical deployment. These attributes make software-first solutions particularly well suited to modernizing under-digitized infrastructure.

III. Investing in Software-First Infrastructure

Investment Criteria

Investing in software-first infrastructure companies requires a structured and rigorous approach, given the operational complexity, regulatory constraints, and historically slow pace of digitization across these industries. When evaluating a new startup in this space, investors typically rely on six core criteria that determine whether a product can scale, deliver measurable value, and overcome the adoption barriers inherent to these sectors.

Market Pain & Urgency

The most important factor is the intensity and immediacy of the problem the software addresses. Many infrastructure operators face high-consequence risks, such as water loss, sewer overflows, equipment failures, grid imbalances, safety incidents, or construction overruns, that impose real financial, operational, and regulatory costs. Labor shortages across utilities and field operations further increase the urgency for automation, especially as experienced workers retire faster than they can be replaced. In parallel, tightening regulatory mandates make compliance non-optional, forcing operators to adopt tools that enhance monitoring, reporting, and resilience. In practice,companies succeed when they address problems operators must solve, not problems they could solve.

Workflow Integration & Adoption Feasibility

Across infrastructure sectors, adoption friction, not technology quality, is the primary determinant of platform success. Utilities, contractors, and facilities teams often rely on long-standing operational routines, and software must integrate seamlessly into these workflows to gain traction (bat). Products need to accommodate field conditions, including offline mobile use, intermittent connectivity, and varying technical proficiency among frontline workers. Because change management is difficult in conservative, understaffed environments, tools that replace paper forms or legacy spreadsheets with minimal disruption tend to win.

Data Defensibility & Proprietary Advantage

Successful infrastructure software companies often rely on proprietary datasets that compound in value over time. GIS layers, underground infrastructure maps, defect-labeled inspection footage, asset condition histories, predictive maintenance models, and operational telemetry all form high-value data assets that competitors cannot easily replicate. As customers use the software, the platform accumulates more operational context, improving predictive analytics and making workflows more reliable. This data flywheel becomes the software’s moat, increasing switching costs and strengthening long-term margins.

ROI Clarity & Quantifiable Savings

Given the nature of their work, infrastructure operators rarely purchase software based on narrative or vision; they adopt tools that deliver measurable savings. Strong products clearly demonstrate reductions in downtime, truck rolls, water leakage, energy waste, rework, or permitting delays (in terms of marketing materials, this would look like a robust set of metric-based case studies). AI-enabled inspection tools reduce manual labor, while workflow platforms minimize errors and increase productivity. Energy or water monitoring systems show direct cost savings that can be calculated on a monthly basis.

GTM Feasibility

The ability to sell and deploy the product is as important as the product itself. GTM dynamics vary widely: water utilities require long procurement processes and pilot phases; construction is highly fragmented and contractor-driven; facilities management often follows mid-market or bottom-up expansion; grid and energy companies require regulatory approvals and multi-stakeholder alignment. Investors therefore prioritize companies with a clearly defined ideal customer profile, repeatable deployment motion, and predictable sales cycles.

Scalability & Deployment Efficiency

Finally, software-first infrastructure companies must demonstrate the ability to scale efficiently across many customers (within their vertical) without extensive customization. Products with standardized integrations (e.g., SCADA, GIS, BIM), simple onboarding workflows, and minimal hardware dependencies scale far more efficiently than tools requiring bespoke implementations. Field usability, configuration speed, and training simplicity all influence scalability. In essence, the product must be deployable across many real-world environments with consistent, reliable outcomes.

IV. VC Entry Points, Valuations & Exit Environment

VC activity in software-first infrastructure follows a characteristic pattern shaped by long procurement cycles, regulatory constraints, complex workflows, and data-heavy product moats. Generally, VCs enter at stages where risk is understood, value inflection points are clear, and adoption can be demonstrated (pre-seed through Series B). Later-stage capital tends to follow only after strong evidence of market pull, multi-site deployments, or strategic relevance to major industry incumbents.

Pre-Seed: Technical Validation & Early Pilots

Pre-seed investments in infrastructure software typically occur when founders are validating the core technology (early AI inspection models, geospatial planning tools, or workflow digitization for field operations). Companies at this stage often run small pilots with utilities, contractors, or facility teams to demonstrate feasibility. Funding is primarily used to refine the product, establish the first customer use cases, and generate early data loops that will later form the foundation of long-term defensibility. VC tend to invest here if there is a strong founder-market fit, clear articulation of high-value pain point, early proprietary data collection, and strong regulatory or operational tailwinds.

Seed: Customer Validation & Early Repeatability

At this point, companies must prove viability beyond a pilot. Investors typically look for the first paying customers, early ARR, and clear evidence that the product fits real-world workflows. For infrastructure sectors, where adoption can be slow, seed rounds often support additional integrations (e.g., SCADA, GIS, BIM), onboarding processes, and development of standardized deployment playbooks. Here, investors tend to evaluate more strongly evidence of consistent usage across field or office teams, sbility to deploy with minimal customization, early defensibility through asset data, inspection data, or workflow metadata, and ROI demonstrated through reduced downtime, leak detection, energy savings, or schedule improvements.

Series A: Product-Market Fit & GTM Scalability

Series A is typically the first major value inflection point for software-first infrastructure companies. At this stage, investors expect repeatable deployments, increasing customer retention, and predictable expansion revenue. Companies usually scale their sales teams, invest in mid-market or enterprise GTM strategies, and deepen integrations with industry-standard systems. Signals of readiness for Series A investment includes 8–12+ institutional customers or multi-site deployment, strong retention and usage patterns, documented improvements in operational efficiency or regulatory compliance, and emerging network effects (e.g., contractors, utilities, or inspection firms pulling the software into new regions).

Series B and Beyond: Category Leadership & Strategic Positioning

Later rounds enable companies to scale nationally or internationally and build the infrastructure required for enterprise-grade reliability. Companies at this stage increasingly attract interest from strategic acquirers, particularly those seeking to expand into digital infrastructure, geospatial intelligence, or AI-enabled operations. Late-stage VCs and strategics look for deep data moats (asset histories, condition data, underground maps, or long-term telemetry), proven ability to integrate with legacy systems at scale, clear expansion into adjacent workflows or verticals, and a lot more financial data.

Exit Environment: Strategic Acquisitions & IPO Potential

Exits in software-first infrastructure tend to be strategic rather than purely financial, driven by vertical incumbents seeking to expand their software portfolios. Acquisitions often occur in the Series B–D range.

Strategic acquirers by vertical commonly include:

Construction: Autodesk, Trimble, Procore

Water/Utilities: Xylem, Arcadis, Jacobs, Bentley Systems, Autodesk

Industrial: Siemens, Schneider Electric, Honeywell

Grid/Energy: Oracle, Itron, GE Digital

V. Market Context (2018 - 2024)

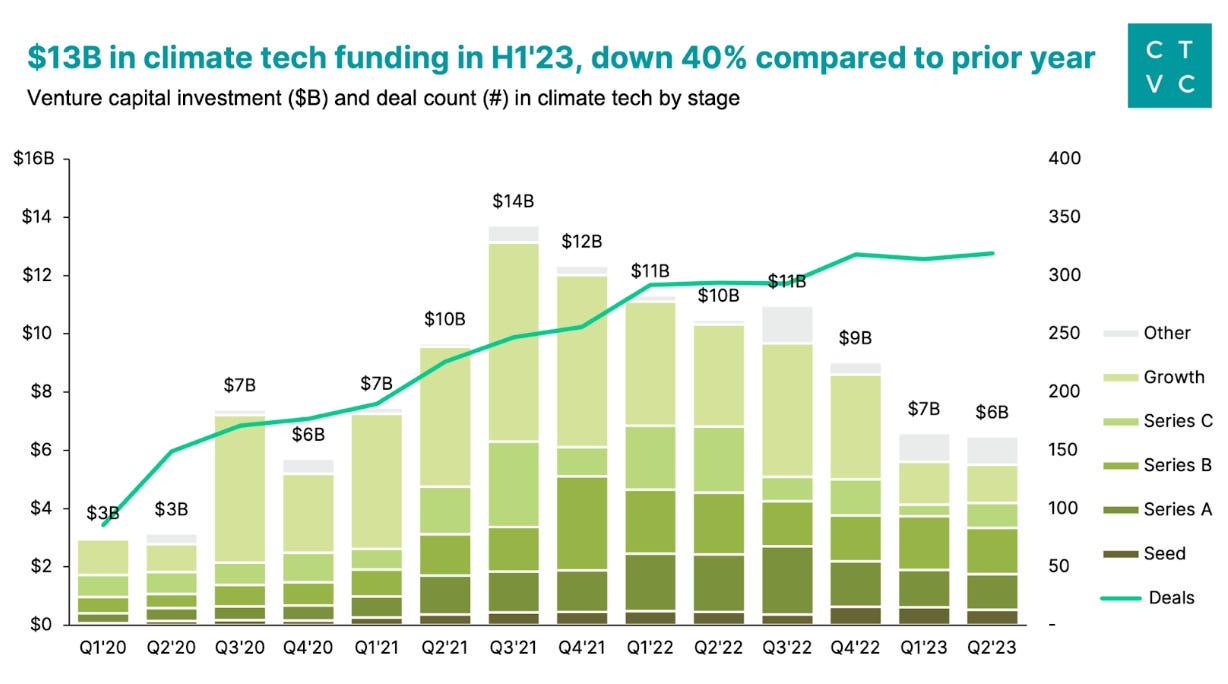

Between 2018 and 2024, investment into software-first solutions for under-digitized infrastructure sectors—particularly construction, water, utilities, and industrial operations—followed a familiar pattern: rapid expansion through 2021, a broad correction in 2022–2023, and early signs of stabilization in 2024. Because most data providers do not track “infrastructure software” as a single category, this section draws on adjacent verticals (construction technology, digital water, grid and energy software, and industrial/Industry 4.0 platforms) as proxies for the broader market for software-first innovation in these sectors. Within those slices, the overall direction is consistent: funding levels peaked around 2021–2022, then reset to a more selective, fundamentals-driven environment where investors favor capital-efficient, software-centric business models.

Deal Volume

Construction Tech Funding Trends

Construction technology (ConTech) is the clearest proxy for software-first innovation in the built environment. Analyses of ConTech funding show a strong rise through the late 2010s and early 2020s, a peak around 2021–2022, and a sharp reset in 2023. Industry reports estimate that global construction tech investment fell by roughly 44% in 2023, from about $5.4 billion in 2022 to $3.0 billion the following year, even as the number of deals slightly increased, indicating more (but smaller) transactions. A 2025 update suggests that construction tech funding rebounded modestly, with total VC inflows rising from roughly $3 billion in 2023 to $3.1 billion in 2024, and deal counts increased from from 236 to 325, pointing to a more active market for digital construction and project-management tools.

Digital Water Market

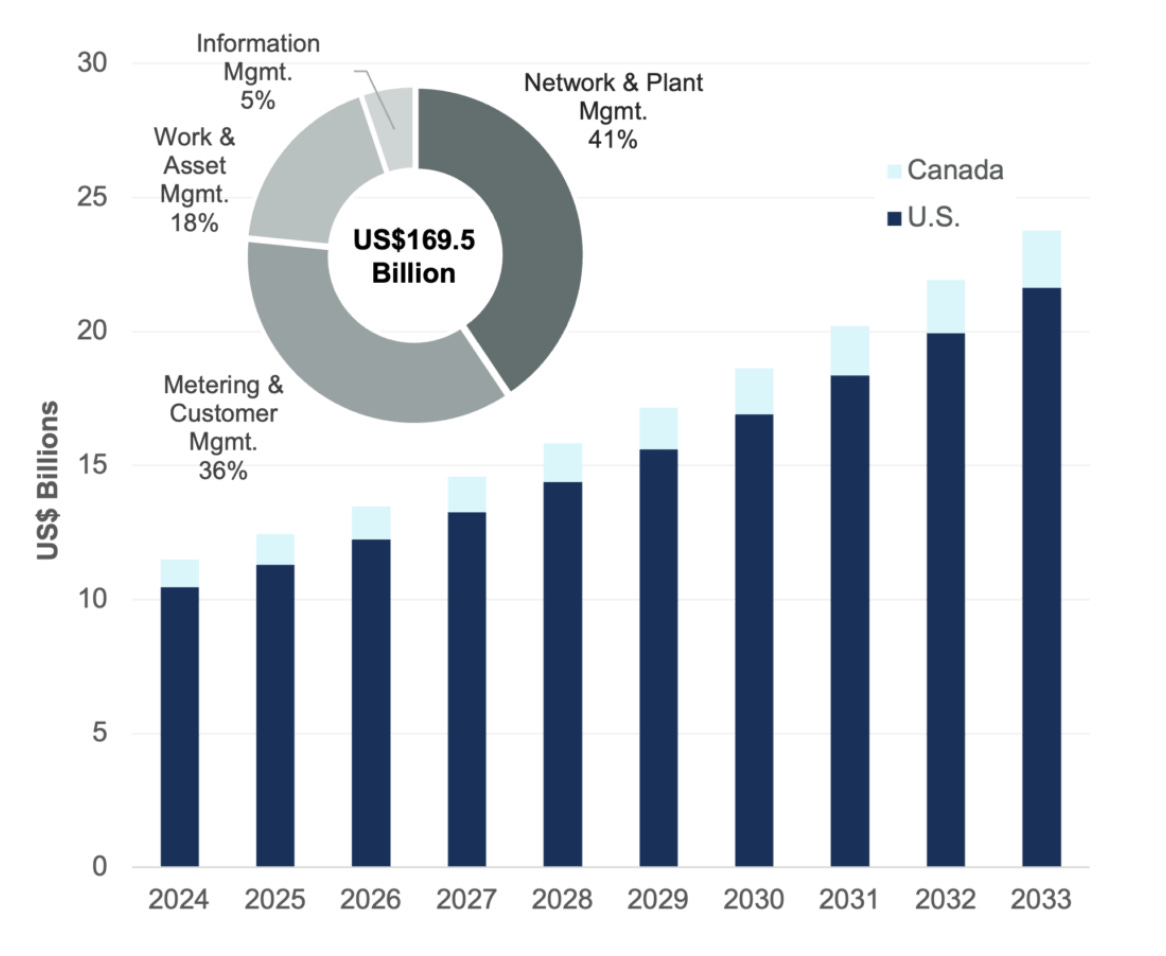

Digital water represents one of the most consistent and resilient areas of software-first innovation within under-digitized infrastructure. Bluefield Research projects that utilities in the United States and Canada will spend $169.5 billion on digital water solutions, including analytics platforms, smart metering, network intelligence, and operational software, over the next decade, indicating a long-term structural demand for digital tools in the sector. Short-term performance data reinforces this momentum: Bluefield also notes that leading digital water vendors reported 6–7% quarterly revenue growth on average, with smart metering companies such as Xylem, Itron, and Badger Meter posting especially strong results. Meanwhile, early-stage activity and consolidation remain steady. According to Bluefield’s Q1 2024 Digital Water M&A Review, merger and acquisition activity in early 2024 remained roughly on par with 2023, indicating continued buyer interest despite broader venture-market pullbacks. Taken together, these indicators show that digital water is a mature and steadily expanding market where software-first platforms continue to gain traction with utilities.

Grid & Utility Software

Software-first innovation in the grid and utility sector has remained robust even through broader venture-market corrections. PitchBook’s grid and energy-transition data shows that grid-infrastructure and energy-transition startups raised $3.5 billion across 197 deals in Q1 2024, a level the report characterizes as “historically elevated” in the post-2021 environment. These companies include grid-forecasting platforms, DER (distributed energy resource) orchestration software, and advanced analytics tools that operate on top of aging utility infrastructure. However, the broader clean energy software and hardware ecosystem has seen a tightening of growth capital. PitchBook notes that overall clean energy VC/PE funding declined again in 2024, with exit value also falling, reflecting a more selective investor environment for later-stage companies. Even with this pullback at the growth stage, early- and mid-stage software companies serving utilities continue to benefit from sustained demand for digital tools that improve grid reliability, enable DER integration, and modernize operational workflows

Industrial Software

Industrial operations and facility management have experienced a steady expansion of software-first tools driven by Industry 4.0 adoption (Industry 4.0 refers to digital, connected, and intelligent systems). Deloitte’s ongoing Industry 4.0 readiness and technology adoption research shows that manufacturers and industrial operators have increased spending on industrial IoT platforms, predictive maintenance software, and operations analytics over the past several years. Companies adopting these tools consistently cite ROI-driven benefits, including reduced downtime, improved equipment reliability, and higher operational efficiency, as primary motivators for digital transformation initiatives. Deloitte’s findings indicate that even in periods of uneven capital expenditure, investments in software-centric maintenance and analytics platforms have remained resilient because they deliver measurable operational savings. For under-digitized sectors such as facilities management and industrial campuses, Industry 4.0 trends provide a reliable proxy for the broader adoption of software-first solutions in mechanical, electrical, and operational environments.

Trends by Stage

No dataset isolates “infrastructure software” as a standalone category, so stage-level trends must be inferred from adjacent verticals (construction tech, digital water, grid software, and industrial/Industry 4.0 SaaS). Across all of these, CTVC, PitchBook, and Carta show the same directional pattern between 2021 and 2024: pre-seed relatively stable, seed/Series A moderately down but still competitive, and Series B+ experiencing the steepest declines.

VI. Key Takeaways

Software-first is the most scalable path to infrastructure modernization.

By layering on top of existing assets rather than replacing them, SaaS, data platforms, and AI tools can reach fragmented customers faster, compound in value as they ingest operational data, and avoid the capex burden of hardware-heavy upgrades.

Under-digitized sectors like water, construction, utilities, and industrial operations are both challenging and attractive.

They suffer from paper-based workflows, aging systems, and regulatory pressure, but those same frictions create large, persistent pain points that make workflow-native, data-centric software especially valuable.

Across verticals, the winning products share the same DNA: workflow fit, data defensibility, and clear ROI.

Whether in digital water, ConTech, grid software, or predictive maintenance, successful companies integrate into day-to-day operations, build proprietary datasets (maps, inspections, telemetry), and can demonstrate tangible savings in downtime, leakage, energy use, or project overruns.

Adoption risk, not technical risk, is the primary gating factor.

Long procurement cycles, conservative cultures, and legacy system constraints mean that investors place outsized weight on GTM feasibility, change management, and the ability to deploy with minimal disruption to field and back-office teams.

Stage dynamics now favor early, capital-efficient execution.

Pre-seed remains relatively stable; seed and Series A are still competitive for teams that can prove workflow fit and ROI; Series B+ capital is reserved for companies that already show category leadership, scalable sales, and robust data moats.

Strategic acquirers, not generic financial buyers, dominate the exit landscape.

Firms like Autodesk, Trimble, Bentley Systems, Xylem, Siemens, Schneider Electric, Oracle, and GE Digital increasingly use M&A to expand their software portfolios, reinforcing the importance of deep integrations and complementary datasets.

For founders and investors, the priority is to build “boring but indispensable” systems of record.

The most durable value in software-first infrastructure will accrue to products that become embedded in critical workflows, own the underlying data model for their niche, and can grow efficiently within (rather than in spite of) the constraints of under-digitized infrastructure sectors.